Profit (or loss) also known as net income (or net loss) are commonly referred to as the bottom line of a company because this figure sits at the bottom of the Profit and Loss statement. Net profit occurs when there is a surplus (or positive amount leftover) after all the expenses of running the business have been deducted from the revenue billed to customers. A loss (or negative profit) can of course incur if expenses are greater than revenue.

Cash flow is another beast entirely.

Positive cash flow occurs when the net amount of cash that flows in and out of a business during a period of time is greater than zero. In a nutshell, it means that the bank account of the business went up during the period because the company’s liquid assets are increasing. And for those of you following along with the Penny and Ernest metaphor, it means that the amount Ernest collected and put into the bank account, exceeded the amount that Penny spent.

KEY POINTS:

- It is possible for a company to have positive cash flow while reporting a loss on the Profit and Loss

- If a company has positive cash flow it means that it’s liquid assets increased over that period of time

- It is entirely possible for a company to post a loss on its Profit and Loss but still have positive cash flow because it received enough cash from borrowing and investing activities to offset the loss for accounting purposes

ANALYSIS:

Net profit or loss from the Profit and Loss statement is merely the starting point for calculating cash flow. Most businesses use something called “accrual accounting”, which means that profit includes revenue and expenses that may be collected or spent at some future point in time and some non-cash amounts. And if these items haven’t (or won’t) hit the bank account, they aren’t relevant to cash flow.

Since the Profit and Loss contains stuff that hasn’t happened yet (or is not relevant to cash), we cannot rely on it solely to make good decisions for the business. We must remove or adjust everything that hasn’t happened yet or is not relevant to cash, in order to get back to a number that represents pure cash flow. Said another way, we are looking to isolate the amount that Penny and Ernest have each run during the period.

To do this in practice, we need to look at the inter-relationship between the Profit & Loss statement and the Balance Sheet. This holistic perspective will give us a true picture of cash flow.

EXAMPLE:

For example, if we were to start from a position where the expenses of a business exceeded revenue (i.e. a net loss or negative income), the most likely result would also be negative cash flow. It is always more difficult to achieve positive cash flow when the business starts from the position of operating at a loss.

However, it is entirely possible to start with a net loss and simultaneously achieve net positive cash flow, but the following scenarios (which are not an exhaustive list) would have to happen in order for that to be feasible:

- The company could receive an influx of cash from either borrowings (i.e. bank debt) or the injection of further equity via investors.

- If the company has a net loss and also a large amount of depreciation expense recorded, the add-back of the depreciation expense (which is a non-cash item since no money leaves the business when depreciation is deducted for tax purposes) could push the company into positive cash flow territory.

- The sale of an asset, or just the reduction in total fixed assets over the period due to depreciation, could also kick up enough cash to help the company record positive cash flow under certain scenarios.

- The collection of receivables (or other money owed) that were posted in a prior accounting period but were collected and put into the bank in the current period is another simple way to push a company into a cash flow positive zone.

- Expenses are recorded on the Profit and Loss when they are incurred, not when they are paid. If a company posts a net loss due to a large amount of accrued expenses (where they were deducted in computing the loss but are not due to be paid until a subsequent financial period), it is entirely possible that the adjustment for these expenses might enable a company to maintain positive net cash flow, despite recording a net loss for tax purposes.

Many in the accounting profession would like to follow their peers who have already made the leap into providing higher-level advisory services to their clients. You may be surprised to discover that according to scientific research, becoming a trusted advisor actually involves a different way of thinking — of using your brain.

Medical science and some high-tech equipment known as functional magnetic resonance imaging (FMRI) and electroencephalograms have greatly enhanced our understanding of how the human brain processes sensory input and makes decisions. These insights have groundbreaking implications for entrepreneurs in general and also those of us in the accounting profession who wish to make the shift from compliance to advisory in the near future.

Neuroscientists have also made great strides in the quest to determine how we can translate these brain insights into workable strategies for boosting individual and organizational effectiveness. Along the way, they have also uncovered surprising correlations between certain patterns of brain functioning (and capability) and the ability to lead and influence others (which are vital skills for all would-be advisors).

Research has proven that the brains of advisors are actually wired differently than those of managers, accountants, or bookkeepers who perform compliance-type tasks. For example, advisors tend to embrace problems and challenges very swiftly and are much more likely to postpone worry and only deal with implications if and when they do occur.

A similar study found that when participants performed exploratory tasks (i.e., looking for new ways to achieve a goal), the ones who used both the left and right sides of their pre-frontal cortex — the region of the brain associated with executive functions — were far more effective. In fact, these neural integrators displayed a far greater capacity to meld right and left side capabilities (blending expressive and creative functions seamlessly with the more rigid, left side cognitive functions) and were more inclined to display decision-making that harnessed both innovation and experimentation.

Conversely, the participants who were more single-mindedly focused on financials and critical thinking (i.e., the stereotypical accountant and bookkeeper), tended to favor the left side of the pre-frontal cortex (the side preoccupied with cognitive behavior, decision-making, language and numbers, and problem solving).

The good news for all those accounting pros with the goal of becoming a trusted advisor is that brain science and neuroplasticity have demonstrated that the brain continues to learn, expand, and develop throughout life, which means it is never too late to rewire your brain for success as an advisor.

Here are four areas of competence that you can develop to materially boost your success as a trusted advisor to your clients.

- Laser-focused Attention

Making the shift to advisory requires an enormous amount of discipline and concentration, as well as the ability to step back and clearly distinguish the forest from the trees. On any given day, there could be 100 or more pressing concerns, client challenges, or opportunities vying for your time and attention. The best advisors stay focused and are not easily sidetracked by bright shiny objects, drama, fear of missing out, or distractions dressed up as emergencies.

Learning to focus your attention like a laser — with varying degrees of intensity, position, direction, and range — is critical for success. However, in order to focus, illuminate, and cut through, your laser needs to be maintained and serviced. The following strategies can help you to hone and enhance your attention:

- Cultivate mental downtime to allow novel solutions and insights to be contemplated and explored fully.

- Good nutrition and ample sleep will also foster better performance and decision-making.

- A technology-free zone at home will allow your mind a chance to rest and recalibrate.

- Mental and Emotional Agility

Being able to draw upon all your internal resources is crucial to enhancing your performance, confidence, resilience, and innovation. Developing the agility and flexibility to weather the storms of advisory is vital to success. This includes both mental and emotional aspects — learning how to regulate, direct, and leverage your thoughts and emotions. Even though we would like to think we are rational decision-makers, neuroscience has proven that decisions are primarily driven by the hasty, automatic, survival-based mechanism of the brain, with heavy influence from emotions, survival instinct, and visual cues.

As such, it is vital to acknowledge and listen to the signals that trigger the primitive part of your brain that decides and acts. Here are some tips you can use to stay connected to both the rational and intuitive aspects of your mind:

- Understand and acknowledge the meaning and purpose behind your work and assist your clients to do the same.

- Become aware of the clients and tasks that drain your physical energy throughout the day.

- Embrace challenges, setbacks, and failures as a natural and valuable part of your journey as an advisor.

- Formally check in with your gut instinct and emotional drivers as equal and valuable partners in the decision-making process.

- Practice the art of shortening your decision-making cycle — document the cost/impact of not making (or delaying decisions).

- Document when you choose to use intuition because the data does not support your gut instinct (and measure how often these decisions are correct).

- Strategic Precision

Neuroscience has proven that we have hundreds of subconscious biases that automatically influence our decision-making. These biases and the beliefs, values, and assumptions you hold at a deeply unconscious level influence and drive your behavior as an advisor far more strongly than rational thought.

Success in advisory requires the ability to step back, challenge your own biases or assumptions, and change your course of action based on rapidly changing circumstances. Strategic precision is achieved when you can step back from your brain’s natural default position (based on those beliefs and assumptions) and consistently make good decisions that help to propel your clients forward.

A study from Stanford underlines the importance of a growth mindset. Essentially, individuals who believe they have unlimited capacity to learn throughout their lifetime outperform those who believe that their intelligence is fixed. What this means is that you can actually learn how to mitigate subconscious biases and assumptions by rewiring the brain patterns that lead to undesired automatic responses when advising your clients.

Here are some great tips that you can use to reduce automatic behaviors that derail your effectiveness as an advisor and learn to manage the inner voice that blocks healthy risk-taking and growth:

- Develop a network of trusted advisors and mentors you can turn to who have diverse perspectives and experience.

- Ask for feedback from colleagues on your strengths and weaknesses regarding decision-making, leadership, risk-taking and innovation, so you can consciously create a plan to grow and develop.

- Practice meditation — brain science has proven that meditation enhances connectivity between both the right and left sides of the pre-frontal cortex, which is essential to success.

- Get familiar with your own default patterns of behavior and formalize an internal alarm bell system that alerts you when you need to stop, review, and reset before taking action.

- Collaboration

Learning how to develop and foster collaboration with your clients is crucial as you make the shift to advisory. Humans are social beings. In fact, brain functioning and neuroplasticity are enhanced by healthy social relationships. Learning how to foster greater accountability, build compassion, and show empathy will increase your ability to engage in healthy risk-taking and support your clients to move forward.

- Create a strong sense of “we” and “team” by creating rituals and rewards that support collaboration with your clients.

- Embed the norm of constructive dissent by letting clients voice their opinions first in meetings and encourage them to challenge your thinking.

- Reinforce the value of experimentation and risk-taking by rewarding those who “fail fast” and are open to learning from their mistakes.

- Exercise compassion and encourage clients to strive for a healthy work-life balance.

Neural integration (connecting different parts of your brain) and neuroplasticity (lifelong learning) increases your growth potential, fosters innovation, helps you manage uncertainty and complexity, and will improve the quality of your relationships.

Accountants and bookkeepers looking to expand into advisory can consciously optimize their brain-mind connection for extraordinary performance, growth, and agile decision-making. Fortunately, all of the capabilities and soft skills that are crucial for your success as an advisor can be learned and mastered with the right training, consistent effort, and a solid plan.

A recent study quantified the incremental revenue opportunity for advisory services in the small to medium enterprise market at $1m per annum, per three hundred clients. For the average accountant or bookkeeper, this is a highly desirable, significant and achievable target. It also explains why there is so much emphasis at industry conferences, in publications and in our training bodies on shifting practices from compliance to advisory services.

Unless you have been hiding under a rock, you know there is enormous pressure to move away from low margin, compliance work — which is disappearing rapidly with the movement of data to the cloud and the introduction of machine based learning. The change is already upon us… it’s inevitable.

However, the challenge remains —> “how do you shift the focus of your practice towards strategic and advisory services”? The proposed shift makes perfect sense in theory, but it also means that you must learn a whole new way to communicate with and market to your clients.

Therein lies the real dilemma…

Thankfully, in most cases, you are already a trusted advisor. However, there is no denying that you face stiff competition from other parties (who are far less qualified) but much better at marketing themselves as having the answers to important questions such as:

- How do I grow my business?

- How do I get more leads and customers?

- How can I use technology to increase my competitiveness?

In this new, highly competitive world of advisory opportunities, you must find unique and valuable ways to solve the big problems that keep your clients awake at night. But here’s the problem — business owners are already overrun with data and spreadsheets they don’t really understand.

An Inconvenient Truth About The Financial Literacy of Your Clients

Last year, we conducted a study with 5000 business owners and discovered, to our dismay, that 93% of them thought they could safely and successfully run their business off only an income statement and aged receivables report each month. They were unable to answer basic questions about the difference between profit, cash in the bank and cash flow. Most also assumed that more customers and sales was the ONLY and best solution to fix a cash flow issue. This research squarely put into focus the seriousness of the financial literacy problem amongst our clients.

Truth is, at least 90% of the entrepreneurs you interact with each day are financially illiterate. They cannot read their financial statements so creating beautiful graphs, dashboards, forecasts or key performance indicators (KPIs), may not be as useful or helpful as you think.

In addition, neuroscience has proven that the part of the brain that makes decisions and acts, struggles to understand numbers and words. It is primarily a visual beast and is strongly influenced by pictures, video, storytelling, strong contrast, emotions etc. This is a huge challenge for us as a profession because most of us have never been taught how to explain financial concepts to our layperson clients, in the language they can understand.

Your clients desperately need strategies to fix the problems that keep them broke and awake at night. They need to know HOW to provide a better living for their families. And you need to find better, more impactful technologies and training to deliver these insights in a way that your clients can actually grasp, digest, and implement.

In a nutshell — “it doesn’t make sense to sell fruit, when what your clients really crave is chocolate.”

Deciphering the Difference Between Fruit and Chocolate

According to Xero’s Make or Break Report in 2015, 65% of business owners blame financial mismanagement for the failure of their business. Most of your clients are in financial pain and searching for the solution that will fix it now. More often than not, this pain will be directly related to cash flow or working capital deficiencies.

They will pay any price for step-by-step instructions to fix this specific problem, but they will only pay pennies for dashboards, KPIs and graphs. Dashboards only diagnose pain. To successfully shift your practice to high margin, advisory services you must go one step further: You must provide a clear path to curing that pain.

The key to building a successful practice in this new, highly competitive world, is to step back and recognize when you might be trying to sell fruit (i.e. dashboards etc. that are meaningful to you) when your client really wants chocolate (i.e. two-three simple, actionable strategies to unlock cash that is trapped in their business).

How Can You Deliver Two-Three Simple, Actionable Strategies?

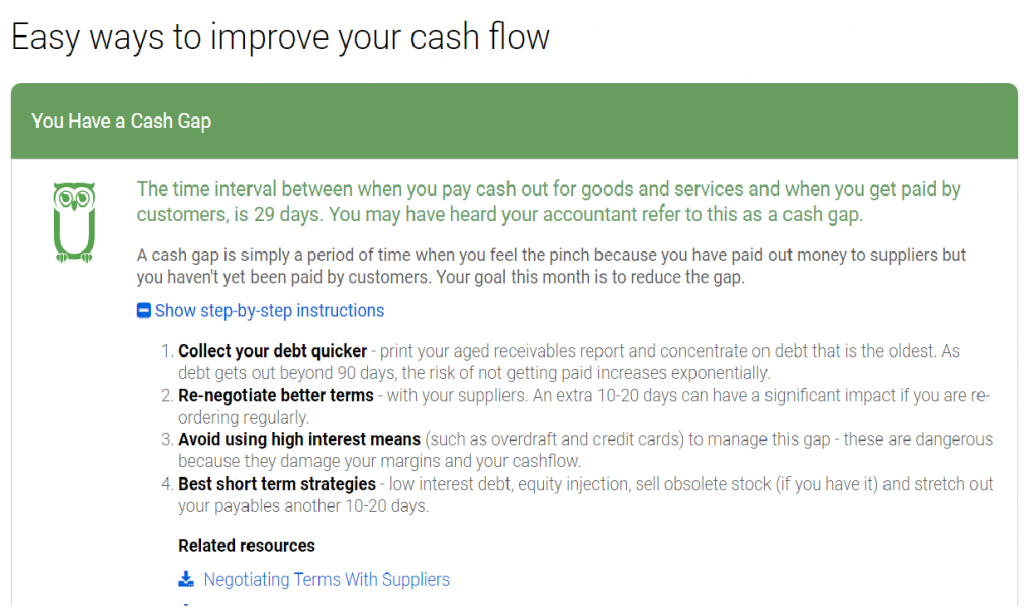

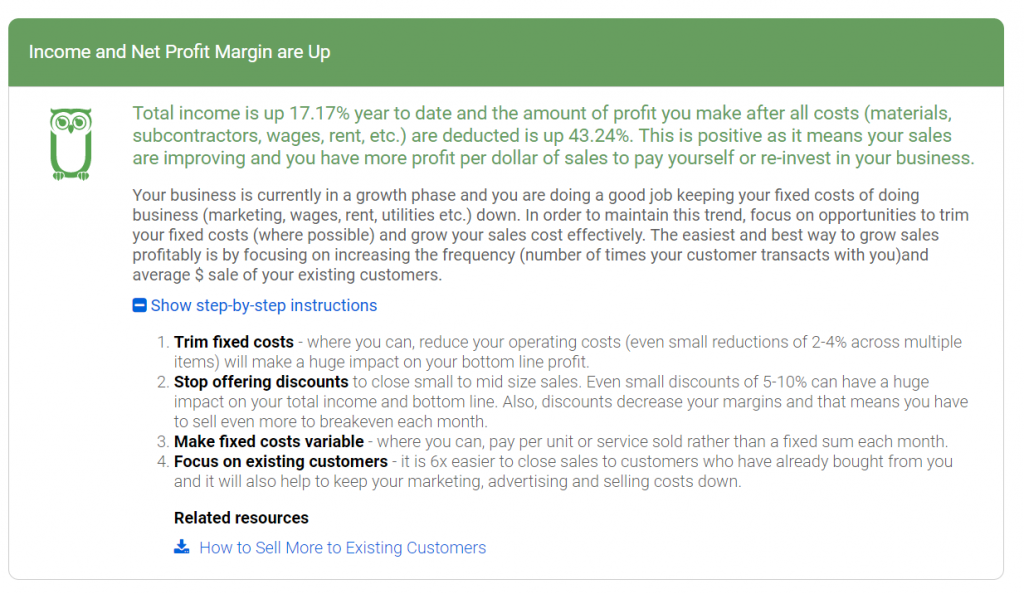

Let’s take for example the case of one of our clients Steve, a commercial tradesman, who makes custom cabinets, counter tops and other kitchen installations for businesses in the hospitality industry. When he came to us, his business was experiencing revenue growth of 17.17% and he couldn’t understand why he was struggling to pay his bills each month.

After analyzing his financial statements, here’s what we discovered:

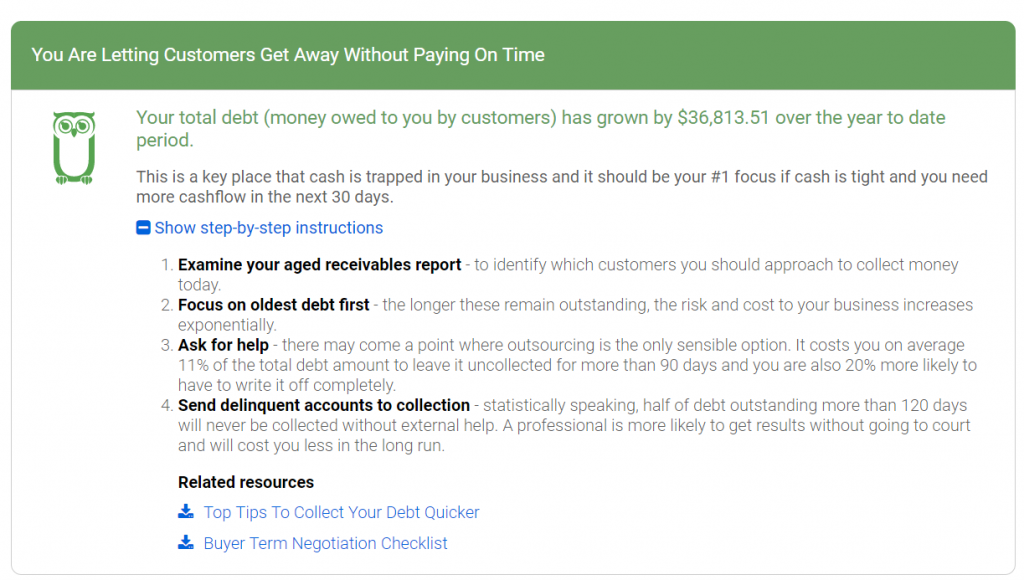

- his total receivables had increased over $36,814 in the six month, year to date period;

- Steve’s customers took on average 29 days to pay;

- while his sales were growing at a rate of 17.17%, his receivables grew at a rate of 131.22%;

- two of Steve’s regular customers were in fact the worst payers; and

- if Steve didn’t make changes immediately to the way he operated his business, his cash balance was going to fall below zero in at least three out of the next twelve months.

Now it would have been easy for us to throw together some beautiful graphs, dashboards and a twelve month cash flow forecast and deliver it to Steve along with our recommendation to “collect your debtors quicker” and “reduce your total outstanding debtors by $36,000 in the next 30 days”.

In fact, the software that we use with all of our clients produces all of these in a matter of seconds.

However, here’s the important point…

If we had done that and simply walked away, there’s a very good chance that Steve would have been in exactly the same position, and possibly even worse off, when we caught up again with him next month. Here’s why…

Steve hates looking at and dealing with his numbers. He often gets the terms receivables and payables mixed up, he is embarrassed to admit that he can’t read the dashboard, and he doesn’t know how to implement the instruction to collect his debt quicker.

While the graphs, KPIs, dashboards and forecasts make perfect sense to you or I, they mean little or nothing to most of your clients. I discovered this the hard way, when I became a business coach eight years ago, after having practiced as a lawyer and chartered accountant for many years. Like most of you, I just assumed that if I simplified the numbers, put them into some sort of context and packaged them up in a way that looked colorful and beautiful, our clients “would surely grasp the insights” and be able to implement strategies to fix the problems.

Truth be told, if we are going to be effective and make a difference, we must do a whole lot more than that. We must not only deliver the “nuggets of chocolate gold” hidden in the numbers, but also present clear strategies and step-by-step instructions so that they can take purposeful action that boosts their bottom line and cash flow.

How Can You Deliver Chocolate & Ensure It’s Still Nutritious?

In the case of Steve, we had to do a whole lot more than just present the KPIs, graphs, and forecasts. In order to make the insights accessible and actionable, we first stripped out all the accounting jargon and showed him in plain language which two or three strategies would have the biggest impact on his cash flow in the next 30 days.

Here is an example of an expert tip and step-by-step instructions that we delivered to Steve. In addition to explaining what the problem was in numerical terms, we gave him a clear explanation that he could refer back to at any time, 4 simple steps to take, and 2 additional coaching resources that he could refer to for guidance on how to implement. These supplemental resources link directly to video training, webinars, photos and case studies which clearly communicate concepts in a way that our clients can grasp.

The key to empowering your clients to take purposeful action often comes down to two simple factors (1) leverage and (2) focus. The quickest way to gain leverage is to quantify the size of the problem and put the cost of continuing to ignore it into perspective. Rather than just instructing your clients to collect debt quicker, you must find new and innovative ways to show them how much they are wasting by continuing to let people get away without paying on time. Similarly, we achieve focus by only presenting the two or three strategies that will have the biggest impact. We avoid overwhelm by pairing back what we share – which in turns allows the client to focus on what is urgent today.

That is the sole focus of our approach – it goes beyond just sharing numbers and metrics and into the realm of coaching and supporting them to fix the financial pain and build businesses that have strong systems and strategies in place to grow safely and profitably.

While the numbers often highlight challenges and opportunities, the solutions are not always limited to the realm of accounting and finance. As our industry evolves, you will no doubt find yourself increasingly asked for advice and support around pricing, technology, systems, sales, marketing and leadership. These are not disciplines which have been traditionally taught to accounting students but the new frontier we find ourselves in, will increasingly demand it of us if we are to remain relevant and valued.

When In Doubt, Find and Sell the Chocolate

Remember, if you client is in financial pain, and most of them are, they will only listen to and pay for insights they can understand and implement immediately. This makes it imperative for you to get to the point quickly and ensure you are delivering only the information (in layman’s terms) that they need to act and cure their pain.

While it’s easy for you to fall in love with beautiful graphs and dashboards, it’s important to remember that they are desperate for clear, simple instructions and tangible strategies that will boost their bottom line and cash flow quickly, cheaply, and easily.

When you take a step back and identify the chocolate each client is desperately searching for, it will also become a whole lot easier to attract more ideal clients, accelerate your growth and profitability, and command a premium price for your advisory services!

For more content on this topic see also Have You Hit This Common Stumbling Block Trying To Shift to Advisory?

While many accounting firms are attempting to offer advisory services, many still aren’t hitting the nail on the head, according to a business coach.

Speaking to Accountants Daily, Businest managing director Rhondalynn Korolak said that accountants are still failing to understand what it is that their clients want. “There’s a common misconception or mistake in the industry where everyone thinks that we have to give dashboards and KPIs to our small business clients. Many simply misinterpret the definition of what advisory services really is (or means).

However, it has statistically been proven that at least 87 per cent of our small business clients are financially illiterate,” she said.

“That’s a huge stumbling block that I think a lot of accountants have to come to grips with. If their clients are financially illiterate, they can’t read their financial statements, so it doesn’t matter how good the graphs look or how beautiful the dashboards and KPIs are. If someone can’t read their financial statements, they can’t read those either.”

Because of this misconception, Ms Korolak said one of the biggest issues plaguing the accounting industry at the moment is that firms aren’t delivering on their clients’ needs.

“The biggest mistake that I see accounting firms making, and even just sole practitioners, is they’re trying to sell fruit to their customers, when what the clients really crave is chocolate,” Ms Korolak said. They attempt to sell their advisory services instead of focusing on helping their clients cure the pain points that keep them up at night worrying.

“Accountants are perfectly poised, they’re perfectly positioned to actually help small businesses, but we can’t do it if we keep trying to teach people accounting. The small businesses owners don’t want to learn it. They want us to take all the accounting jargon out and give them a clear roadmap with step-by-step instructions of how they’re going to fix their problems.”

Ms Korolak believes this comes down to a skill gap created by universities still teaching outdated skills and a lack of training opportunities.

“Advisory services aren’t about dashboards and it isn’t about giving people reports and all that kind of stuff. It’s about two things: getting leverage on the client and getting them to take action,” she said.

“The skills that most advisors would need to be able to pull that off and do it well are in many ways the exact opposite of skills that we were trained in school.”

This article originally appeared in the Accountants Daily on May 1, 2017

Rhondalynn Korolak is the founder of businest and the co-founder of Make The SHIFT

Our industry is full of people who have worked hard to build their practices or reach upper management. They’re intelligent, highly skilled, and hardworking. But only a handful have reached the pinnacle in our industry and attained the mantle of ‘the trusted advisor’ in the eyes of their clients.

Why is that? Interestingly, it is only subtle nuances that separate those stand-out performers from the rest.

It has often been said that ‘what got you to here won’t get you to there’, and if you think about it, this premise makes a lot of sense because if the skills that you currently have are capable of establishing you as the trusted advisor, then most of your income will be coming from strategic and advisory services.

Right now, there are a handful of success breakers (workplace habits or skills shortages) that are holding you back from making the next big leap forward. The key is to identify what those are and discover some practical solutions you can use to make the next big leap.

Let’s examine one of the most common success breakers in our industry and the implications it has for you as you move your practice away from compliance and toward strategic and advisory services: withholding information.

This is the refusal to share information in order to maintain an advantage over others.

For a very long time, accountants and bookkeepers have been the gatekeepers of the most vital knowledge in business – financial literacy. Cloaked in jargon, rules that take years to master, and systems that obfuscate financial performance, we have inadvertently created an industry shrouded in fear and mystery.

Most of what accountants do on a daily basis is incomprehensible to a lay person, and for many decades we have gotten paid well because we are in possession of this mysterious yet valuable commodity.

When I speak to accountants and bookkeepers about educating their clients in plain language, one of the most common objections that I hear is, “But if I teach my client how to understand their financial reports, they won’t need me anymore”. Unfortunately, too many have bought into the mindset that keeping clients in the dark is an essential ingredient to maintaining relevance and value.

This argument holds no water when held up to careful scrutiny. It makes no more sense to perpetuate this mindset than it does for a parent not to teach their child how to walk, use utensils, read or graduate from diapers to the toilette. Our job is to support, teach and nurture our clients to become the best and most successful versions of themselves, not to hold them back for fear they won’t need us.

Education enables understanding and growth, and growth is vital to the health of each small business, your practice and the whole economy. As your clients’ understanding and competency grows, so do the complexity of the problems they are confronted with. This growth allows them to turn to you for more challenging, strategic and interesting advice.

Cloud accounting and machine learning are also breaking down those purpose-built walls of specialised accounting knowledge and putting more information, insights and power directly into the hands of our lay person clients. As a result, there is a very real possibility that your job today, as you know, it is going to go away and be replaced by something else.

That is the sole reason why thought leaders, industry bodies and training organisations are urging you to focus on becoming ‘the trusted advisor’. But that mandate is both misleading and elusive.

Our entire industry and the way we educate and train new recruits are focused on technical skills, legislative changes, and GAAP processes. From day one, you are taught to speak to your clients in terms of financial statements, key performance indicators, reconciliations, and forecasts. That is your language and your domain of expertise, not theirs. No matter how colourful or beautiful your reports are, they are still incomprehensible to most of your clients who have never studied accounting and don’t wish to do so.

When you sit down to advise your clients, it’s easy to fall into the trap of ‘explaining accounting’, as opposed to focusing on the specific steps and strategies that your client needs to implement to grow profitably. There is very little training in university, on the job, or in industry bodies to show you HOW to become ‘the trusted advisor’. But unfortunately, there is an overwhelming and distracting emphasis on social media, apps, sales, and marketing.

However, you marketing yourself as ‘the trusted advisor’, no matter how convincingly, doesn’t make it so. It isn’t a designation that we declare ourselves, but rather an honour and a privilege our clients bestow upon us for curing the pain points that keep them up at night.

Becoming ‘the trusted advisor’ is about connecting with your clients and communicating in a way that inspires and empowers them to take action to improve their results. The skills to achieve this are more in line with coaching and training, than sales or marketing.

Where to from here?

If you don’t accept the premise, that your job as you know it is about to change drastically, then you do not need to do anything. You may simply sit back and watch as more and more of what you do is replaced by cloud technology and apps.

However, doing nothing is rarely a viable option in any business or industry. Change is inevitable. It is already upon us.

What got you here – to the success and accomplishments you have already achieved – is not going to get you to where you need to be as our industry continues to evolve rapidly.

Right now you are facing an uncertain future. What that means is that traditional approaches, such as hiding behind the complexity and jargon of our industry, are unlikely to be helpful. In order to evolve and remain relevant despite the changes, you must find a new set of tools, skills, talents and behaviours that complement the ones you already have, not replace them.

Here is a list of strategies that you can use to identify and acquire the new tools, skills, talents and behaviours that will catapult you to the pinnacle of our industry and enable you to become even more successful this year:

1. Specify in writing your targets for growing the advisory services of your practice. These targets must be written down in order to be effective, compelling and measurable.

2. Identify one or two specific niches of clients that you will focus on this year to achieve those targets.

3. Create a list of the two to three most important pain points that these clients have right now (the things that worry them and keep them up at night).

4. Identify and document the key strategies and steps that your clients must take in order to cure the pain points and prevent them from recurring again next month.

5. Critically evaluate the reports, dashboards, metrics and graphs that you present to your clients. Remember, your clients are not accountants and they have no desire to learn accounting. They merely want you to help them fix the problems so they can make more money while doing what they love.

6. Identify and develop the materials that you need to gain leverage on your clients and empower them to take action. When in doubt, ask for advice from trusted colleagues who have proven experience delivering impactful advisory services. It pays dividends to work collaboratively with your colleagues and it also means that you avoid ‘reinventing the wheel’.

7. Be open to trying new things (this includes technology, processes, communication styles, delivery channels, etc). It is only by trial and error that you will uncover what works and what doesn’t.

8. Identify the new skills, talents and behaviours that are needed by every member of your team, and the courses or programs that will help you achieve those results.

9. Create a comprehensive budget for training over the next 12 months and a formal plan for evaluating the progress and competency of each team member. Money spent on your team’s skills to deliver effective solutions is far more impactful than advertising and social media.

10. Start tracking the progress of each client to ensure they are following through on the action plan discussed with them.

11. Open a dialogue with your clients, ask for specific feedback from them about what they have learned, how it has impacted their business, and what you could do better.

This article originally appeared as an interview with Lara Bullock on Accounting Daily website.